Third Sector Trends in England and Wales tracks charities’ financial health

Howard Lake | 21 January 2026 | News

The latest Third Sector Trends in England and Wales 2025 report reveals a voluntary sector grappling with persistent financial disparities, changing donor-funder relationships, and a dramatic flight from public service contracting.

The findings of Third Sector Trends in England and Wales 2025: income sources, assets and financial

wellbeing underscore the need for strategic agility in a financially demanding environment.

Third Sector Trends has been surveying the voluntary, community and social enterprise sector every

three years since 2010. This is its sixth iteration.

Advertisement

You can download the latest report in PDF at no charge.

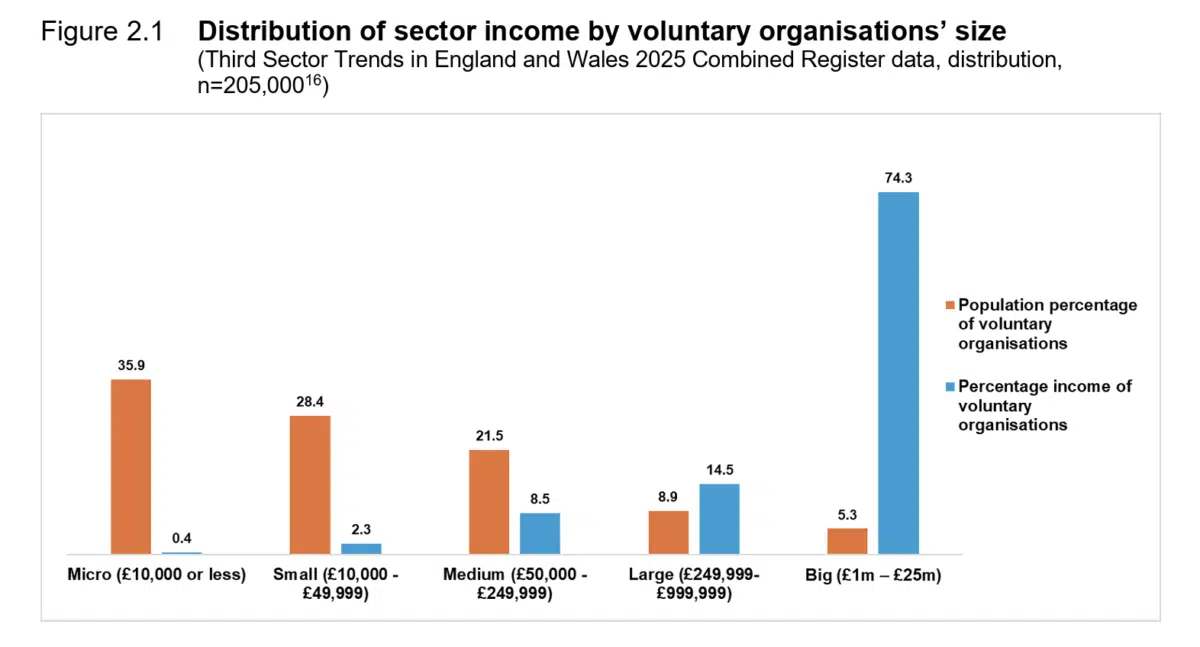

Uneven distribution of income to the sector

While the sector’s total estimated income is substantial, its distribution is anything but equitable. The report confirms that micro organisations, which constitute 36% of the sector’s population, receive less than 1% of the total income.

Conversely the largest 5% of organisations command a huge 74% of sector income. This deep inequality confirms that the financial wellbeing of the sector cannot be viewed through a single lens, as size is the dominant factor in access to resources.

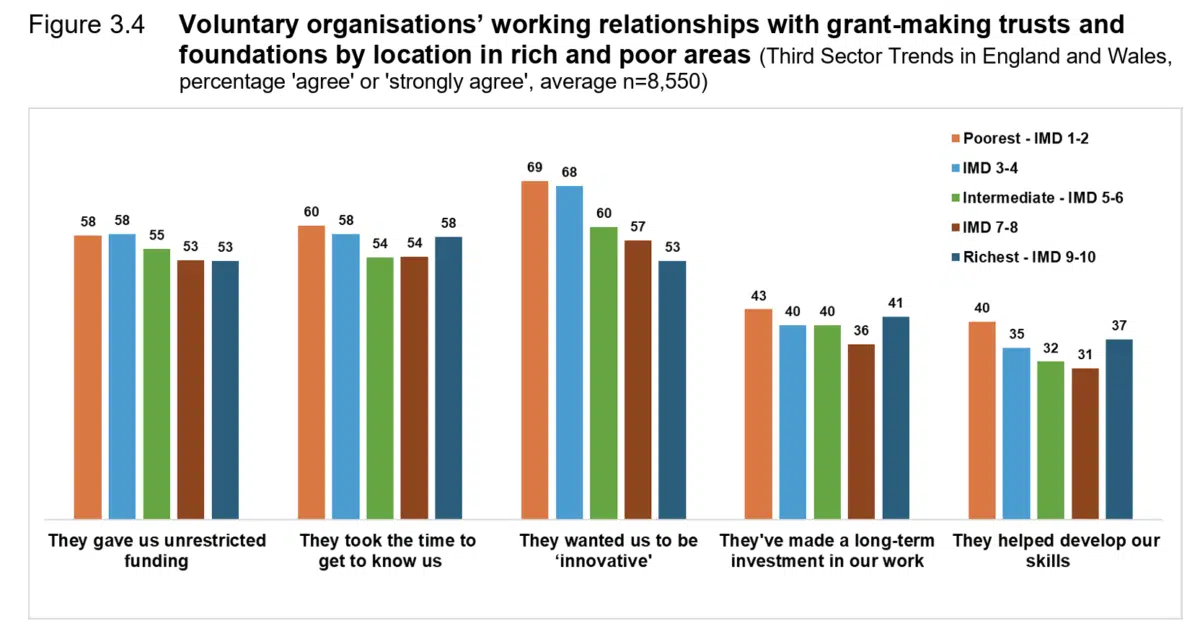

Grants are more valued but restricted

Grant funding is still the most highly valued income source in relative terms, a trend that has strengthened over the past 15 years, moving away from previous ‘grant dependency’ narratives.

Some grantmakers appear to have sustained some of the more flexible practices adopted during the pandemic:

- Unrestricted funding: although slightly down from the pandemic peak of 60% in 2022, 56% of third sector organisations (TSOs) still report receiving unrestricted or ‘core’ funding – an incrfease from the 46% pre-pandemic level in 2019.

- Long-term investment: the percentage of TSOs receiving long-term investment has risen substantially to 40% in 2025, up from about 31% before and during the pandemic.

- Innovation returns: Pressure from grant-makers for TSOs to be ‘innovative’ has bounced back sharply to 62% (up from 50% during the pandemic), signaling a return to pre-pandemic requirements for “novelty and demonstrable impact”.

The contracts crisis deepens

The trend of voluntary organisations withdrawing from public service delivery contracts continues, with steep declines across all size bands.

Among the biggest TSOs (income £5mn-£25mn), participation has fallen to 50% in 2025 from 64% in 2019.

The main culprit remains the low value of tenders, which are failing to cover rising delivery costs, exacerbated by hikes in the National Minimum Wage.

The report notes that government efforts to ‘smooth’ procurement are missing the point; the core issue is contract value. This trend challenges the notion of ‘social enterprise’ enthusiasm from policymakers, as earned income is also weakening, particularly among newer organisations.

Financial health and outlook

The sector’s financial wellbeing is secure for a majority, but vulnerabilities are concentrated.

While most TSOs (82%) hold reserves, 27% have used them for essential costs like rent and wages, a figure that rises to 33% in the least-affluent areas.

This confirms that ‘struggling’ TSOs – those with falling income and no or emergency-used reserves – are overwhelmingly located in the most deprived communities (14% there vs. 6% in the richest areas).

The sector’s financial outlook has grown less optimistic. Only 28% of TSOs expect their income to rise over the next two years, down from 36% in 2019.

The message is clear: while the sector’s largest and newest organisations show signs of thriving, leaders must navigate a contraction in contract work and a competitive, though supportive, grant environment, all while managing resources against the backdrop of persistent regional and area-based financial fragility.

For sustainable growth, a renewed focus on private giving, subscriptions, and investments – which are valued more highly in affluent areas – will be crucial, alongside advocating for fair-value public service contracts.

About the research

Third Sector Trends was established by Northern Rock Foundation in 2008 and is “the largest and longest-running empirical study of the sector in the UK”. It is now run by Community Foundation North East and St Chad’s College, Durham University.

The analysis is underpinned by a dataset of 205,000 organisations drawn from the full range of registers of nonprofit organisations so that survey evidence can be scaled-up reliably to produce credible and

convincing findings on sector activities.

It is designed to complement rather than replicate findings from the NCVO UK Civil Society Almanac, Charity Commission and 360 Giving.

In 2025, its survey which closed on 30th September received a national and fully representative sample of over 8,680 responses from across England and Wales.

The project is funded in 2025-26 by Community Foundation North East, Lloyds Bank Foundation

England and Wales, Wales Council for Voluntary Action and Millfield House Foundation.

Further analysis of the findings from the survey will be released over the next six months on separate topics including:

- The contribution of the voluntary sector to place: a study of North East England in comparative

context (February 2026) - Sustaining organisational vitality and community impact (March 2026)

- Latest Third Sector Trends report reveals insights into nonprofits’ political activity at local level (15 February 2023)

Related posts

Lloyds TSB Foundation for England and Wales increases grants in first half of 2012

New funding strategy announced by Lloyds Bank Foundation for England and Wales

Lloyds Bank Foundation to give £3m to tackle domestic abuse

A.F. Blakemore launches 1917 heritage grants scheme

![]()

About Howard Lake

Howard Lake is consultant editor of UK Fundraising. He founded the site in 1994 and successfully sold it in 2022. As director of Giving X Ltd he is exploring growing giving on a massive scale.

He is the founder of Fundraising Camp and co-founder of GoodJobs.